Last updated: May 29, 2026

5 min read

The global homeschooling industry is transitioning from a peripheral education alternative into a structurally integrated segment of the broader K–12 ecosystem.

Between 2026 and 2040, the market is projected to demonstrate sustained double-digit expansion in several regions, underpinned by digital transformation, regulatory liberalization in selected jurisdictions, micro-school proliferation, and AI-powered personalized learning infrastructure.

Based on consolidated projections from industry research and extrapolated long-range CAGR modeling:

- Global homeschooling market (2026): Estimated between USD 4.8–6.5 billion (core curriculum and digital services segment).

- Expanded ecosystem valuation (including platforms, co-ops, EdTech integrations, tutoring, testing services): USD 20–30 billion+ in 2026.

- Projected 2040 global market cap (base case scenario): USD 65–95 billion, depending on regulatory, technological, and demographic trajectories.

- Long-term CAGR (2026–2040): 8%–12% globally; 12%–18% in high-growth Asia-Pacific markets.

This article provides a structured breakdown by region, country, segmentation, and macroeconomic drivers shaping the homeschooling capital landscape through 2040.

1. Defining the Homeschooling Market

For analytical precision, the homeschooling market includes:

- Digital Curriculum Providers

- Learning Management Systems (LMS)

- Assessment & Accreditation Services

- Hybrid/Micro-school Platforms

- Tutoring & Supplemental Instruction

- Community and Support Networks

- AI-Personalized Learning Systems

This excludes traditional public or private schooling budgets and focuses specifically on home-based or parent-directed education expenditures.

2. Global Market Size Outlook (2026–2040)

2.1 2026 Baseline

Recent industry modeling from multiple market intelligence sources suggests:

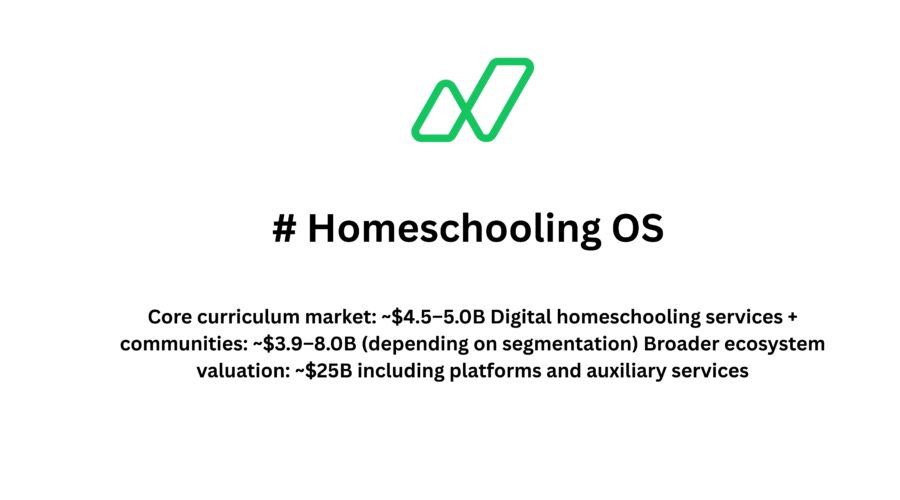

- Core curriculum market: ~$4.5–5.0B

- Digital homeschooling services + communities: ~$3.9–8.0B (depending on segmentation)

- Broader ecosystem valuation: ~$25B including platforms and auxiliary services

Given normalization post-pandemic but sustained elevated participation, 2026 represents a structural plateau rather than a peak.

Estimated Global Market Capitalization – 2026

| Segment | Estimated Value (USD) |

|---|---|

| Curriculum & Learning Materials | 4.8B |

| Digital Platforms & LMS | 6.5B |

| Tutoring & Services | 5.2B |

| Hybrid & Micro-schooling | 4.0B |

| Total Addressable Market (TAM) | ~20–25B |

2.2 Growth Trajectory to 2040

Applying conservative CAGR scenarios:

- Low-growth scenario (8% CAGR): ~$65B by 2040

- Base case (10% CAGR): ~$78B by 2040

- High-growth (12% CAGR): ~$95B+ by 2040

Acceleration drivers include:

- AI-powered adaptive learning

- Cross-border curriculum licensing

- Decentralized accreditation frameworks

- State-funded homeschooling subsidies (U.S., Canada, Australia trends)

- Growth in micro-schools and community pods

3. Country-Wise Market Forecast (2026–2040)

3.1 United States

The United States remains the largest homeschooling market globally.

- ~4 million homeschooled students (2024–2025 estimates)

- Participation rate: ~8–10% of K–12 population

- Strong state-level funding mechanisms (ESAs, vouchers)

2026 U.S. Market Size:

Estimated USD 12–15 billion (full ecosystem valuation)

2040 Projection:

USD 35–45 billion

Drivers:

- Education Savings Accounts (ESAs)

- Rise of AI-integrated platforms

- Cultural shift toward educational sovereignty

- Growth of micro-schools

The U.S. is expected to retain ~40–45% global market share through 2040.

3.2 Canada

Homeschooling is legal nationwide and moderately expanding.

2026 Market:

~USD 1.2–1.8 billion

2040 Forecast:

~USD 4–6 billion

Drivers:

- Provincial flexibility

- Hybrid online learning programs

- Rural access advantages

3.3 United Kingdom

The United Kingdom has experienced steady post-pandemic normalization but remains above pre-2020 levels.

2026 Market:

~USD 1.5–2.2 billion

2040 Forecast:

~USD 5–7 billion

Drivers:

- Dissatisfaction with standardized schooling

- Growth in digital-first families

- Increased deregistration trends

3.4 Germany

Homeschooling remains illegal under strict compulsory attendance laws. However, alternative education markets (private tutoring, digital supplements) contribute indirectly.

2026 Direct Homeschool Market:

Near zero (formal)

Indirect Digital Supplement Market:

~USD 800M–1B

Unless federal reforms occur, growth remains constrained.

3.5 Australia

Australia shows strong CAGR in the homeschooling ecosystem.

2026 Market:

~USD 10–15 million (direct homeschooling registration services segment)

Expanded ecosystem likely ~$300–500M including platforms and tutoring.

2040 Forecast:

~USD 1–1.5 billion ecosystem-wide

Drivers:

- State registration compliance

- Rural digital adoption

- Parental autonomy movements

3.6 India

India is a high-growth opportunity region.

While formal homeschooling numbers are modest, digital curriculum adoption is accelerating.

2026 Market:

~USD 1–2 billion (digital + alternative education platforms)

2040 Projection:

~USD 8–12 billion

Drivers:

- Competitive exam pressure

- Low-cost online curriculum

- English-medium demand

- Rapid EdTech penetration

India may become the second-largest homeschooling-adjacent market by 2040.

3.7 China

Homeschooling remains heavily regulated. Growth is concentrated in:

- International online curricula

- Hybrid international learning pods

- Digital tutoring

2026 Market:

~USD 2–3 billion (alternative + digital self-directed learning)

2040 Forecast:

~USD 10–15 billion (if regulatory climate softens)

3.8 Japan & South Korea

Both countries show rising dissatisfaction with high-pressure academic systems.

Combined 2026 Market:

~USD 1.5–2.5 billion

2040 Forecast:

~USD 6–9 billion

Drivers:

- Mental health awareness

- Digital-first youth adoption

- Government tolerance of flexible pathways

3.9 Latin America (Mexico & Brazil)

Growth remains nascent but promising.

2026 Combined Market:

~USD 800M–1.2B

2040 Projection:

~USD 4–6B

Key growth factors:

- Private school affordability issues

- Expanding middle class

- Online curriculum imports

3.10 Middle East

Selective growth in UAE and private expatriate communities.

2026 Market:

~USD 500–800M

2040 Projection:

~USD 2–4B

4. Regional Market Share Projection (2040)

| Region | Estimated Share 2040 |

|---|---|

| North America | 45% |

| Asia-Pacific | 30% |

| Europe | 15% |

| Latin America | 6% |

| Middle East & Africa | 4% |

Asia-Pacific will be the fastest-growing region by CAGR.

5. Market Segmentation Evolution (2026–2040)

5.1 AI-Powered Personalization

By 2030+, AI-driven adaptive learning engines will likely account for 25–35% of market value.

5.2 Micro-Schools

Community-based micro-schools are expected to:

- Expand in suburban North America

- Capture 10–15% of homeschooling-related capital by 2040

5.3 Accreditation & Credentialing Platforms

Cross-border digital accreditation services may become a $5B+ segment by 2040.

6. Macro Drivers Influencing 2026–2040 Market Cap

- Technological Democratization

- Parental Sovereignty Movements

- Urban Safety Concerns

- Customization Demand

- State-Level Funding Mechanisms

- Demographic Shifts

- AI-native learning environments

7. Risk Factors

- Regulatory crackdowns (Europe, parts of Asia)

- Reintegration into public systems

- Economic recession reducing discretionary spending

- Over-commercialization fatigue

8. Strategic Outlook for Homeschooling OS

For platforms such as Homeschooling OS, the 2026–2040 horizon presents:

- SaaS scaling opportunities

- AI integration pathways

- Cross-border licensing expansion

- Government partnership potential

- Hybrid micro-school infrastructure support

The addressable market expands substantially if positioned not merely as a homeschool tool, but as a decentralized education operating system.

9. 2040 Scenario Modeling

Conservative Scenario:

- Global TAM: $65B

- U.S. Dominance continues

- Asia-Pacific moderate acceleration

Transformational Scenario:

- Global TAM: $95B+

- India + U.S. dual leadership

- AI-native education mainstreamed

- Government subsidy normalization

10. Conclusion

The homeschooling market from 2026 to 2040 is positioned for sustained structural growth rather than temporary cyclical expansion. It is evolving into a technology-enabled, globally distributed educational alternative.

By 2040:

- The industry could approach $80–95 billion globally.

- Asia-Pacific will rival North America in growth velocity.

- AI and micro-school ecosystems will redefine segmentation.

- Regulatory landscapes will determine market ceilings.

Homeschooling is no longer a marginal pedagogical choice—it is a parallel education economy.

For investors, EdTech builders, and policy analysts, the 2026–2040 window represents one of the most significant structural shifts in K–12 education since the digitization of higher education.